KiwiSaver funds are often categorised as conservative, balanced or growth funds.

These are based on two main things: time horizon and risk appetite.

Time horizons relate to how long people want to hold their investment before they put that money to another use. Time horizons often change as people grow older and their goals evolve. Some may be looking to use their KiwiSaver investment to help buy a first home in the next few years, while others want to use their investments to fund a comfortable retirement in a few decades.

Time horizons can affect risk appetite, or the amount you’re willing to see your investment fluctuate over a period.

Riskier investments can lead to higher returns over the long term, but they tend to move up and down in value to a greater extent over the shorter term. A longer time horizon can help smooth out any higher fluctuations associated with riskier funds, which can result in a higher overall return.

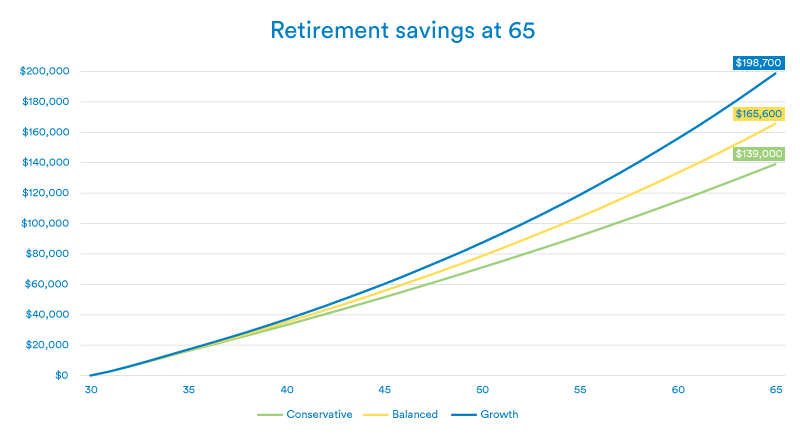

Growth funds tend to experience greater fluctuations in value whereas conservative funds could help reduce the risk of your investment dropping in value dramatically before you want to use it. Balanced funds sit somewhere between these two.

At Booster, we offer a variety of funds designed to match different time horizons and risk appetites.

All our funds come with a suggested minimum investment timeframe and risk indicator (a measure of volatility of returns over a five-year period) to give you a quick overview of the type of fund it is. Whether you're looking at stepping into a home in the next few years or setting yourself up for retirement, we're here to help you assess and make the best choice.

Conservative funds

Designed for people who will need access to their savings shorter term – from zero to 4 years plus depending on the specific fund. The idea is your savings balance is less likely to fluctuate significantly but won’t make as much in the way of returns.

Balanced funds

Designed for people who will want access to their savings in about 5-6 years plus depending on the specific fund. The idea is your savings may fluctuate from time to time but over the medium term will potentially make higher returns than a conservative fund.

Growth funds

Designed for people who will want access to their savings further down the track - in 7-15 years and longer depending on the specific fund. The idea is your savings may go up and down due to the nature of the market but will potentially make higher returns than a balanced fund in the long-run.

So, what should I do from here?

Making sure you’re in the right fund is probably one of the best things any of us can do to make sure we’re on track. After all, every bit counts when aiming for a relaxing, financially resilient life in retirement.

You can get an idea about what type of fund may be right for you by taking our quiz. You can also talk to your financial adviser or book a free account review with Booster today.

Call on 0800 336 338, email kiwisaver@booster.co.nz or book a call for your account review.

Choosing the right type of fund for you could be the difference between tens or even hundreds of thousands of dollars. It’s probably worth taking a few minutes now to check if you’re in the right fund.

Share this article

-

Note – This blog provides general information only and is not, and is not intended to be financial advice for the purposes of the Financial Market Conduct Act 2013.

*Calculation Assumptions

Industry-standard forecast rates of annual return (after fees and tax at 28%) as set by the FMA, across four main fund types – Conservative 2.5%. Balanced 3.5%, Growth 4.5%. Corrected and updated as of 21/05/2024.

No savings suspension or withdrawals take place

We’ve assumed an annual salary increase of 3.5%, a 3% employee contribution rate and a 3% employer contribution rate.

Your annual government contribution entitlement amount is received each year, up to a maximum of $521.43. This figure is not adjusted for inflation.

Fees, tax rates and government contributions are assumed to continue unchanged until you reach age 65.

All projected balances are in today’s dollar terms (by adjusting for the impact of inflation at 2% per annum).

Booster Investment Management Limited is the issuer of the Booster KiwiSaver Scheme (Scheme). The Scheme’s Product Disclosure Statements are available at www.booster.co.nz or by contacting your financial adviser.